China, Chips, and Chaos: Where Smart Investors Are Putting Their Money Now

As geopolitical tensions rise and global supply chains shift, investors around the world are focusing on one of today’s most important industries: semiconductors. China is working hard to become self-sufficient in chip technology, whereas the U.S. is attempting to prevent the export of advanced chips in order to maintain its technological advantage. All this is happening while artificial intelligence (AI) advances at a rapid pace.

These factors are creating a fast-moving, risky, but potentially lucrative market for investors. Amid the chaos, savvy investors prefer long-term stability to distraction. Here are two stocks that show where true innovation and resilience lie:

Rising Star #1: Qualcomm

Valued at $174.4 billion, Qualcomm (QCOM) develops and sells advanced semiconductors and wireless technologies, primarily for mobile phones, automotive systems, Internet of Things devices, and AI applications. It is best known for its Snapdragon processors.

QCOM stock is up 3% year-to-date.

Qualcomm’s robust second quarter showcased the strength of its business model. Qualcomm reported a 15% increase in adjusted revenues to $10.8 billion year over year, with adjusted earnings of $2.85, representing 17% growth. The majority of this strength stemmed from the company’s chip business, the Qualcomm CDMA Technologies (QCT) segment, which generated $9.5 billion. This was driven by strong growth in automotive (up 59%), IoT (up 27%), and handsets (up 12%). The Qualcomm Technology Licensing (QTL) licensing business contributed another $1.3 billion to overall revenue.

Qualcomm continues to dominate the premium mobile market with its Snapdragon 8 Elite platform, which is regarded as one of the world’s most powerful smartphone chipsets. Its Snapdragon X platform is also rapidly expanding into the PC market, to surpass its goal of 100 designs by 2026. Beyond mobile, Qualcomm is aggressively expanding into automotive, with the Snapdragon Digital Chassis platform helping it reach $8 billion in automotive revenue by fiscal 2029. Extended Reality (XR) is emerging as another growth driver, aided by Snapdragon technology and collaborations with Meta Platforms (META) and Samsung. The company intends to generate $2 billion in XR revenues by fiscal 2029.

Qualcomm returned $2.7 billion to shareholders via dividends and buybacks, showing strong free cash flow generation and management confidence. The company has also committed to returning 100% of free cash flow to shareholders this fiscal year, citing strong fundamentals and a scalable model.

Concerning China, Qualcomm continues to be a key player in the Chinese smartphone ecosystem, where local subsidies have increased flagship shipments. Management stated that the company’s Q3 guidance takes current tariffs into account, also admitting that the trade landscape remains dynamic. Qualcomm has also taken steps to diversify its business, both geographically and across sectors, to reduce its reliance on a single region or product category.

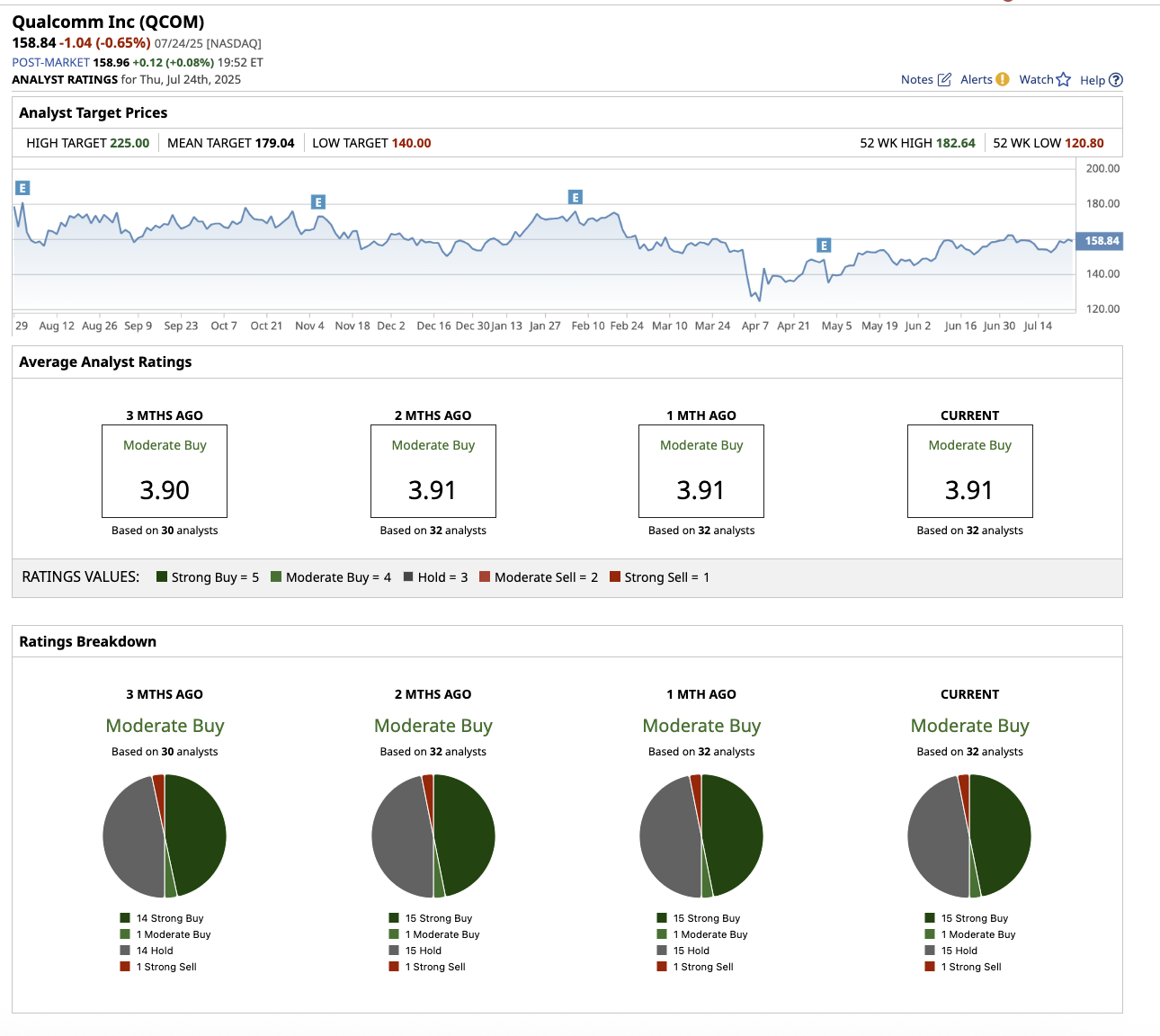

Overall, Wall Street rates QCOM stock a “Moderate Buy.” Out of the 32 analysts that cover the stock, 15 rate it a “Strong Buy,” one suggests a “Moderate Buy,” 15 rate it a “Hold,” and one rates it a “Strong Sell.” Its average target price of $179.04 suggests an upside potential of 13% from current levels. Its high target price of $225 implies a potential upside of 42% in the next 12 months.

Rising Star #2: Broadcom

Valued at $1.3 trillion, Broadcom (AVGO) designs, develops, and distributes a wide range of semiconductor and infrastructure software products. Its diverse portfolio includes networking chips, enterprise storage, broadband, and wireless communication. Broadcom also provides enterprise software solutions for cybersecurity, storage, and mainframes.

AVGO stock is up 24.8% year to date, outperforming the broader market.

Broadcom reported staggering revenue of $15 billion in the second quarter, up 20% year over year. AI semiconductor revenue soared to $4.4 billion, up 46%, marking nine consecutive quarters of consistent growth. This growth was driven by custom AI accelerators (chips designed for specific hyperscaler clients) and AI networking, which account for 40% of AI semiconductor revenue. Management confidently forecasts 60% AI revenue growth in Q3 2025, which is expected to continue into fiscal 2026, cementing AI semiconductors as its long-term growth driver.

Furthermore, software is no longer a side hustle for Broadcom. It has strengthened its position in software through strategic acquisitions such as VMware for $69 billion, which officially closed in 2024. Its infrastructure software segment generated $6.6 billion in revenue, up 25% YoY, accounting for 44% of total company revenue. Over 87% of Broadcom’s top 10,000 customers now use VMware Cloud Foundation (VCF).

Furthermore, the company is converting customers from perpetual licenses to subscription-based ARR, resulting in more predictable revenue. Looking ahead, major cloud players are expected to continue to invest, demand for training and inference workloads will rise, and software adoption will remain strong, painting a positive long-term outlook.

Broadcom is not only growing rapidly, but also profitably. Adjusted earnings increased 44% to $1.58 per share in Q2. The company also generated $6.4 billion in free cash flow, paying out $2.8 billion in dividends and $4.2 billion worth of share repurchases.

Despite rising U.S.-China tech tensions, Broadcom is well-positioned to thrive. It does not rely heavily on high-end GPUs with export restrictions.

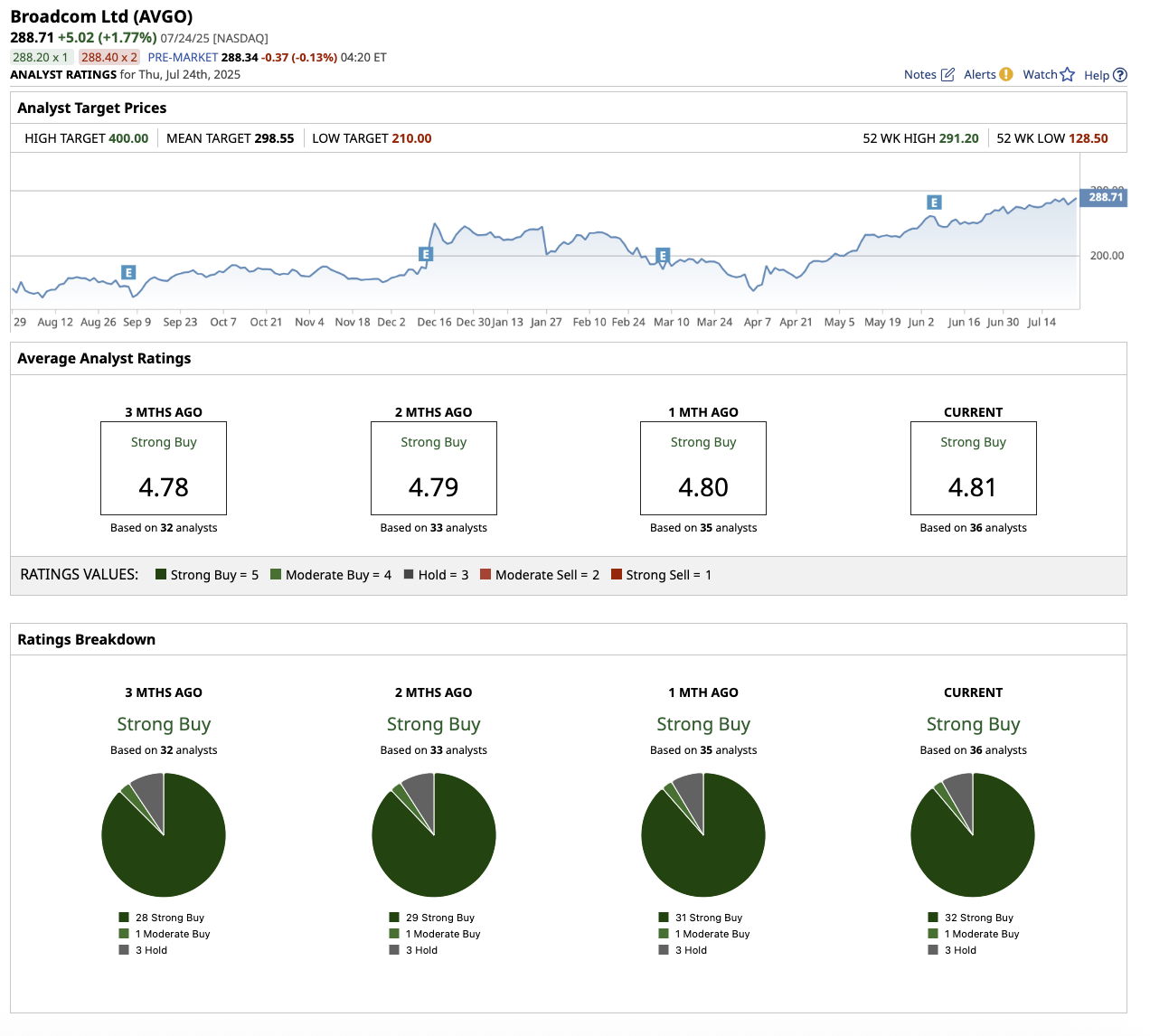

Overall, Wall Street rates AVGO stock a “Strong Buy.” Out of the 36 analysts that cover the stock, 32 rate it a “Strong Buy,” one suggests a “Moderate Buy,” and three rate it a “Hold.” Its average target price of $298.55 suggests an upside potential of 3% from current levels. Its high target price of $400 implies a potential upside of 38% in the next 12 months.

The Key Takeaway

No doubt, the U.S.-China chip war presents significant challenges. Export controls, shifting alliances, and technology bans may all cause short-term turbulence. However, the best way to profit from the semiconductor boom may be to invest in companies that can adapt, endure, and grow in uncertain times. Both Qualcomm and Broadcom serve this purpose.

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.